You get the email on a Tuesday afternoon. Counsel needs bank records for a fraud matter, the client only has partial statements, and the hearing calendar won't wait for anyone's filing mistakes. The legal team talks about subpoenas. You're the one who'll ultimately have to make sense of whatever the bank sends back.

That's where the accounting workflow usually breaks down. Lawyers focus on authority, service, and objections. CPAs focus on completeness, transaction detail, and how to turn a pile of PDFs into something usable for tracing, reconciliation, and damages work. The subpoena of bank records sits right in the middle of those two worlds.

If you're the CPA, forensic accountant, or legal support professional handling the records after service, you need more than a legal definition. You need a process that reduces rejection risk on the front end and cleanup work on the back end.

What Is a Bank Record Subpoena

A subpoena of bank records is a formal legal command requiring a bank or other financial institution to produce specified documents. In practice, the typical reference is to a subpoena duces tecum, which is a subpoena for records or things, not live testimony.

For a CPA, the important distinction is this. A subpoena is not a courtesy request, not an authorization form, and not a vague demand for “all banking records.” It's an enforceable document request that has to match the governing rules of the case.

Why banks treat these requests formally

Banks don't release records because someone sounds urgent. They release records when the request fits a recognized legal pathway and the paperwork is complete. That's why a subpoena feels less like asking for documents and more like presenting the bank with the exact credentials required to open a restricted file.

Historically, this formal structure became much clearer after the Right to Financial Privacy Act of 1978, enacted after the Supreme Court's 1976 decision in United States v. Miller. The Office of the Comptroller of the Currency explains that the RFPA requires federal authorities to use specific legal tools, such as customer authorization, administrative subpoena or summons, search warrant, judicial subpoena, or a formal written request when no subpoena power exists, and in most cases to provide written notice to the customer. The OCC's bulletin also explains that customers generally receive the purpose of the request and instructions for protecting the information, which is why bank production isn't handled as an informal records release (OCC bulletin on financial privacy procedures).

Practical rule: If the request isn't procedurally valid, the bank's records department usually won't “work with you.” It will reject, delay, or escalate the request.

What the subpoena means for the accounting team

Once the subpoena is valid, your job starts long before records arrive. You should already know:

- Which accounts matter: Operating, payroll, merchant, escrow, personal, or linked savings.

- Which time period matters: A narrow period often gets faster compliance and cleaner review.

- Which record types matter: Statements, deposited items, checks, wire details, signature cards, account opening documents, and correspondence don't all serve the same purpose.

- What format will be usable: A thousand pages of image PDFs can be legally sufficient and still create major accounting friction.

If you're dealing with support work for assurance or investigative matters, it helps to think about subpoenaed records the same way you think about evidence collection in an engagement. You're not just gathering documents. You're preserving a defensible chain from request to analysis. That same discipline shows up in broader audit support workflows for financial records.

Navigating the Legal Requirements

The legal framework matters because the subpoena's usefulness depends on whether the bank has to honor it. A well-drafted request with the wrong authority, wrong court, or wrong notice process can waste days.

CPAs don't need to litigate the subpoena. But they do need to spot when the legal team is asking for something operationally impossible or procedurally weak.

Who can issue the subpoena

The answer depends on the type of matter. In practice, bank records may be sought in civil litigation, criminal investigations, administrative matters, or forfeiture proceedings. The issuing authority and service rules can differ sharply across those settings.

That's why “send the subpoena to the bank” isn't a useful instruction by itself. You need to know the forum, the issuing party, and whether the subpoena is tied to a case already filed.

Federal and state rules are not interchangeable

A good example is 18 U.S.C. § 986, which authorizes subpoenas duces tecum to financial institutions after the commencement of certain federal forfeiture actions, including actions under 18 U.S.C. §§ 1956, 1957, and 31 U.S.C. §§ 5322 and 5324. The statute also requires that all parties be notified when such a subpoena is issued and preserves ordinary civil discovery under the Federal Rules of Civil Procedure (federal forfeiture subpoena statute).

That tells you two practical things. First, subpoena power can be highly context-specific. Second, notice requirements are often built into the process, so surprises are less common than clients assume.

A state-law example shows the same point from a different angle. Virginia's § 19.2-10.1 governing subpoenas for banking and credit card records is marked effective until July 1, 2026, with a replacement version effective July 1, 2026 in the same statutory material linked above. Procedure changes. Forms change. Effective dates matter.

The constraints CPAs should check early

When counsel asks you to prepare the record categories, these are the legal process questions worth confirming before anyone drafts exhibits or transaction schedules:

| Issue | Why it matters operationally |

|---|---|

| Issuing authority | A bank may reject a document that lacks proper authority |

| Jurisdiction | The subpoena may need to conform to the court or state where compliance is required |

| Customer notice | Production timing may depend on notice and objection periods |

| Scope | Broad language creates more objections and more useless data |

| Preservation needs | Some matters require immediate follow-up for additional record classes |

The fastest subpoena workups usually come from teams that narrow the ask before they argue about the law.

For the accounting side, this is similar to tax document collection. You want the request to match the task. If the legal team wants tracing of transfers, ask for transfer support. If they want a cash proof, ask for complete monthly statements and deposited item detail. If the matter overlaps with filing support, document collection discipline from bank statement review for taxes carries over well.

Privacy and objection are part of the process

Clients sometimes assume a subpoena means the bank will automatically turn over everything. Often, that's not how it works. Notice can trigger objections, motions to quash, or negotiated narrowing of the request.

For the CPA, that means timing assumptions need to be conservative. Don't schedule your reconciliation work as if production will arrive immediately or in a clean package.

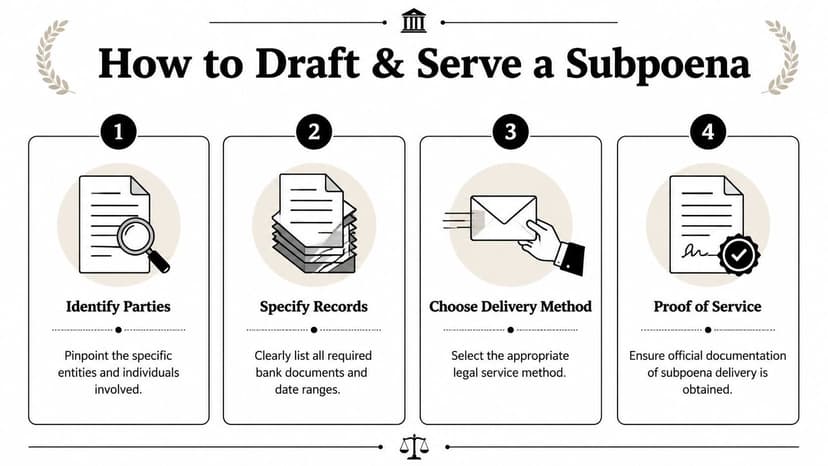

How to Draft and Serve the Subpoena

Most avoidable delays often begin due to certain factors. Banks don't reject subpoenas only because the case is weak. They reject them because the request is sloppy, the scope is too broad, or service was done incorrectly.

The accounting professional's role here is simple. Help draft a request that a records department can understand and fulfill without guessing.

What to include in the request

The best subpoenas for bank production read like an indexed pull list. They identify the account, the period, and the exact document classes.

A practical request usually works better when it specifies:

- Named account holder: Include legal entity name and known aliases if relevant.

- Account identifiers: Use full account number if authorized, or partial number plus institution and account type.

- Date range: State a start date and end date, not “from inception to present” unless there's a real reason.

- Record categories: Monthly statements, check images, deposit slips, wire records, ACH detail, signature cards, account opening records, and correspondence should be listed separately.

- Delivery instructions: Identify where and how production should be sent, and who may receive encrypted material.

Most bank subpoena failures are boring. Wrong service. Vague scope. Missing paperwork.

What does not work

A request for “any and all records” across multiple years might sound thorough, but it usually creates delay. Banks scrutinize relevance and scope. Narrower requests tend to produce fewer objections and less back-and-forth.

The same goes for service. In federal civil matters, Rule 45 requires personal delivery. The article discussing best practices notes that “serving a subpoena requires delivering a copy to the named person,” so email, overnight mail, or certified mail alone is typically insufficient in that setting. The same discussion also notes recurring state-level failure points, including wrong serving method, overbroad requests, and omission of required fees or proof-of-service steps, and gives California as an example where a business-records subpoena workflow requires a clerk-issued subpoena and completed proof of service (bank subpoena service and scope best practices).

A working checklist for service

Different jurisdictions vary, but this pre-service review catches many common problems:

Confirm the forum rule

Use the governing civil, criminal, or administrative rule set. Don't assume state and federal service mechanics are interchangeable.Verify the recipient

Large banks often have designated subpoena processing addresses or legal response units. Sending it to the branch manager usually slows things down.Attach required paperwork

Proof of service, witness fees where required, clerk issuance where required, and any consumer notice forms should be checked before service.Document the handoff

Keep service details organized because the records department may ask for proof before release.

A capable support person can save a lot of attorney time here. If your firm needs extra hands for document prep, service coordination, or production tracking, Paralegal Assistants can be a useful resource for overflow work.

A short explainer can help orient junior staff before they handle service logistics:

A model request style

Instead of:

- any and all records relating to defendant

Use:

- monthly statements for checking account ending in XXXX from January through June

- front and back images of all cleared checks during that same period

- deposit item detail and deposited check images

- outgoing and incoming wire transfer records

- ACH transaction detail

- signature card and account opening documents

That version gives the bank something it can route, search, and produce.

Reviewing and Reconciling Bank Production

When the bank finally responds, the production usually looks less polished than anyone hoped. You may get password-protected files, scanned PDFs, mixed orientations, duplicate pages, or records split across several transmissions. Sometimes the statements are complete but the supporting items are not.

That's normal. It's also where accounting discipline matters more than legal drafting.

First review before any data entry

Don't start keying transactions the moment the files arrive. First compare the production against the subpoena request and the transmittal from the bank.

Look for these mismatches:

- Missing periods: One statement cycle absent in the middle is common.

- Missing page sequences: Large statements often arrive with skipped image pages.

- Missing record classes: Statements may be produced without check images or deposit support.

- Unreadable scans: If amount fields or transaction descriptions are blurred, the data can't be trusted.

- Duplicate productions: Supplemental transmissions may repeat prior files without saying so.

If opening and closing balances don't roll from one statement to the next, assume the production is incomplete until proven otherwise.

Reconciliation logic that saves time

A simple continuity test catches a lot. Take the closing balance from one statement and confirm it matches the opening balance on the next. If it doesn't, stop and identify whether the issue is a missing statement, a special account event, or a scan problem.

Then review transaction density. If one month appears unusually thin compared with surrounding periods, that can signal omitted pages or a partial export.

Here's a practical intake table many forensic teams use:

| Review item | What to verify |

|---|---|

| Statement sequence | Every month requested is present |

| Balance continuity | Prior closing matches next opening |

| Page count integrity | No visible skips or cut-off pages |

| Record class completeness | Statements plus requested supporting items |

| File naming | Consistent labels for later exhibit use |

If the matter involves fiduciary or pooled funds, your review should be even tighter. A good template for managing client trust accounts can help structure the reconciliation side when trust-style controls or three-way matching logic are relevant.

Build an exception log

The best habit here is an exception log, not a memory game. Track each missing period, unreadable page, duplicate file, and follow-up request in one place. That log becomes your support for supplemental subpoenas, meet-and-confer discussions, or declarations about incomplete production.

When balances don't tie, a focused process for reconciliation mismatches in financial records helps keep the issue analytical instead of anecdotal.

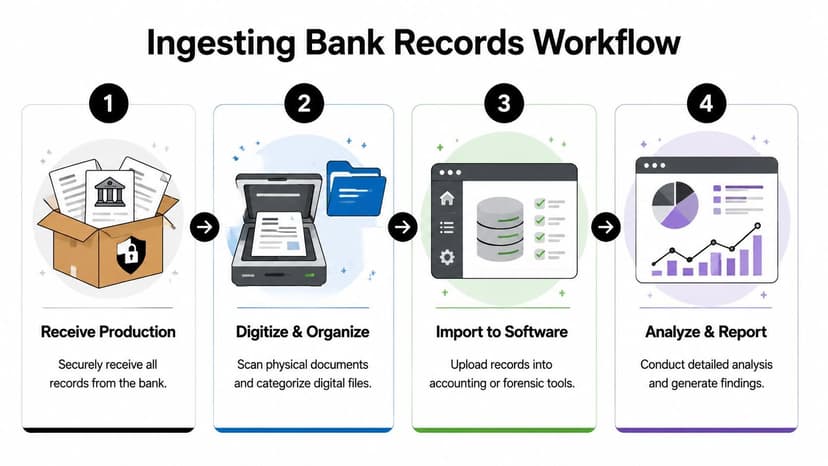

Ingesting Subpoenaed Records into Your Workflow

The legal side ends when the records arrive. The accounting burden starts there.

Most subpoena productions are not analysis-ready. They're evidence-ready. That's a big difference. Evidence-ready means the bank has produced records in a defensible form. It does not mean your team can immediately sort, filter, pivot, trace, or import the data into working papers.

The old workflow versus the workable workflow

The old method is familiar. Open PDF. Zoom in. Type dates and amounts into Excel. Fix OCR mistakes manually if someone already tried a scanner. Repeat for every month, every account, every supplemental production.

That method creates three recurring problems:

- Manual transcription risk: A single transposed digit can throw off a tracing schedule.

- Inconsistent categorization: Different staff members normalize descriptions differently.

- Poor scalability: The workload gets worse fast when multiple accounts or entities are involved.

A better workflow uses structured intake from day one. Organize files by institution, account, date range, and production batch. Keep the original production untouched, then create a working copy for extraction and analysis.

A practical ingestion sequence

This is the process that tends to hold up under expert review and internal quality control:

Lock the originals

Save the original PDFs exactly as produced. Don't rename them so heavily that you lose the bank's original identifiers.Create a processing index

Map each file to account holder, account type, statement period, and production source.Extract transaction data

Convert records into structured rows that can be reviewed, sorted, and reconciled.Run tie-outs

Compare extracted totals and balances back to the source statements before using the data in schedules.Export for the destination system

Some matters need Excel for tracing. Others need CSV or direct accounting import.

Clean ingestion matters more than flashy analysis. If the underlying rows are wrong, every chart and summary built on top of them is wrong too.

Tool selection matters more in legal-accounting work

General OCR tools can pull text from a PDF, but bank records have layout issues that make generic extraction unreliable. Statement formats vary by bank. Deposits and withdrawals may appear in different columns. Running balances can be misread. Multi-page records can split transactions awkwardly.

That's why legal and accounting teams should evaluate software based on how it handles bank statement structure, not just whether it “reads PDFs.” If you're comparing options, a broader roundup of top legal tech tools can be useful for the litigation side, but accountants still need a workflow that respects statement math and import requirements.

If your destination is bookkeeping or cleanup work after forensic review, compatibility with QuickBooks bank data import workflows becomes important. The less reformatting your staff has to do after extraction, the fewer downstream errors you create.

What a CPA should insist on before analysis

Before you build a cash flow, a source-and-use schedule, or a transfer tracing model, confirm that your dataset is:

| Requirement | Why it matters |

|---|---|

| Searchable | You need to isolate payees, memo strings, and transfer references |

| Structured | Dates, descriptions, debits, credits, and balances should live in separate fields |

| Reconciled | The extracted data should tie back to statement balances |

| Preserved | Original files and processed outputs should both be retained in an orderly file set |

Once those conditions are met, the work becomes normal accounting again. You can sort related-party transfers, identify round-dollar activity, match deposits to invoices, and isolate unknown disbursements without fighting the file format every step of the way.

Common Questions about Bank Subpoenas

What if the bank is in another state

Treat that as a procedure issue first, not a mailing issue. The subpoena may need to comply with the rules of the state where the bank or records custodian must respond. Don't assume your home-state form can be sent across state lines and enforced.

From the accounting side, the practical response is to flag this immediately for counsel before you promise a production timeline.

How much does it cost to subpoena bank records

There's no single answer. The cost usually comes from a mix of attorney time, service costs, bank response fees where permitted, follow-up correspondence, and your team's review time after production.

The hidden cost is often the accounting cleanup, not the legal paper itself. A narrow request can reduce that burden. A vague request tends to multiply it.

What if the bank sends incomplete records

Don't patch around the gaps and hope no one notices. Build an exception list, identify exactly what's missing, and ask for a targeted follow-up. In many matters, a short, precise supplemental request works better than arguing broadly that the production was inadequate.

What if my own bank records are subpoenaed

Get legal advice quickly. A subpoena can raise privacy, scope, objection, and timing issues that need counsel review. From a records standpoint, preserve what you have and don't alter files, labels, or related communications.

What should I ask counsel before I begin analysis

Ask five things:

- What issue are we trying to prove or disprove

- Which accounts are in scope

- What period controls

- What form of output is needed

- Whether production is considered complete

Those answers prevent wasted analysis.

Can extracted transaction data replace the original statements

No. Use extracted data as a working dataset, but keep the original statements as source evidence. In expert work, you'll often need both. If your team is routinely converting raw statements into usable spreadsheets, it helps to standardize bank statement data extraction workflows so every case starts from the same intake process.

If you routinely receive subpoenaed statements as PDFs and need them turned into clean, review-ready spreadsheets, ConvertBankToExcel is built for exactly that accounting workload. It helps CPAs and finance teams convert bank records into structured Excel, CSV, and accounting-ready files while preserving a clean path from source document to analysis.