Auditing a bank isn't just about checking boxes for regulators. It’s the process of independently digging into a financial institution’s records, controls, and day-to-day operations to make sure the numbers are right, risks are managed, and laws are being followed.

Think of it as a critical health check, not just for the bank, but for the entire financial system it's a part of.

Why Auditing in Banks Is More Than Just Compliance

A bank is a massive, incredibly complex machine that juggles billions of dollars in public funds. Auditing in banks is the mechanism that keeps that machine balanced, stable, and worthy of trust. It goes way beyond a simple compliance task—it's the very foundation of financial integrity and public confidence.

I like to think of a bank auditor as an expert navigator on a giant container ship. Their job is to meticulously chart a course through treacherous waters, spotting the hidden risks that could sink the whole operation. These aren't just obvious icebergs; they're subtle threats like a slow-burning internal fraud scheme, a tiny but critical gap in operational controls, or a major compliance issue that everyone else overlooked.

The Two Pillars of Bank Audits

The audit function is almost always split into two distinct roles. They complement each other, and understanding how they differ is key to seeing the whole picture.

Internal Audit: This is the bank's own in-house team, acting as a constant first line of defense. They're on the ground every day, monitoring internal controls, evaluating how efficiently things are running, and making sure daily activities follow the bank's own policies. They report their findings directly to the bank's board and senior management.

External Audit: These are the independent, third-party CPA firms hired to give an unbiased opinion on the bank's financial statements. Their work is what gives shareholders, regulators, and the public confidence that the numbers being reported are fair and accurate. Their independence is everything.

The real point of auditing a bank isn't just to find mistakes that have already happened. It’s to strengthen the institution against risks that haven't surfaced yet. It gives the board the assurance it needs to make big strategic bets and gives regulators the confidence to know the bank is operating safely.

This two-pronged approach creates a powerful system of checks and balances. The internal team handles the real-time monitoring and continuous improvement, while the external team provides that objective, periodic validation from the outside.

For any CPA, finance professional, or business owner who works with the banking sector, this structure is fundamental. The game is always changing, and it's worth reading a new playbook for the modern bank audit to understand its growing strategic role. The responsibility is immense—a single oversight can ripple through the entire economy.

Stepping into a bank audit feels less like a typical accounting job and more like entering a high-stakes world run by powerful regulators. This isn't just about checking boxes. It’s a live environment where a single misstep can trigger serious consequences for the bank, all designed to protect depositors and keep the financial system stable.

Think of the rules as layers of security. Each one—from federal laws down to specific agency guidelines—is there to catch a different kind of risk, whether it's a massive institutional failure or a single employee's misconduct.

The Key Regulators and Their Roles

For any bank in the United States, a few key agencies are always watching. They set the rules for audits, and while each has its own focus, they work in concert to make sure nothing slips through the cracks.

- The Office of the Comptroller of the Currency (OCC): The OCC is the boss for all national banks and federal savings associations. Their main job is to ensure these banks operate safely and follow the law to the letter.

- The Federal Deposit Insurance Corporation (FDIC): The FDIC is famous for insuring our deposits, but it's also the main federal regulator for state-chartered banks that aren't part of the Federal Reserve System. This makes them a huge player, especially in community banking.

- The Federal Reserve System (The Fed): As the nation's central bank, the Fed regulates the biggest players—bank holding companies and state banks that are members of its system. Its ultimate goal is keeping the entire financial ecosystem from wobbling.

These agencies show up for routine examinations, usually every 12 to 36 months, based on the bank’s size and risk profile. When they issue an audit finding, it isn't a friendly suggestion. It’s a direct order that requires a fast and comprehensive fix.

Foundational Laws Shaping Modern Audits

Underpinning the regulators' power is a set of landmark laws, most of them born from a past crisis to prevent history from repeating itself.

The real point of these laws isn't just to verify numbers. It's to force transparency and hold people accountable. They push auditors to look beyond the balance sheet and scrutinize risk management, board oversight, and the bank’s entire culture.

Two laws, in particular, dictate a huge portion of any modern bank audit:

- The Bank Secrecy Act (BSA): This is the country's main defense against financial crime. The BSA forces banks to help the government detect and stop money laundering. Auditors spend a massive amount of time testing a bank's Anti-Money Laundering (AML) program, especially its process for filing Suspicious Activity Reports (SARs).

- The Sarbanes-Oxley Act (SOX): Passed after the Enron and WorldCom scandals, SOX created incredibly strict rules for public companies. For banks, this means a grueling assessment of internal controls over financial reporting, putting senior executives on the hook for the accuracy of their numbers.

Getting this stuff wrong isn't a simple paperwork mistake. It can lead to crippling multi-million dollar fines, business restrictions, and a hit to a bank's reputation that can be impossible to recover from.

The New Focus on Tech and Third-Party Risk

The regulatory world never sits still. Recent updates show a major pivot from old-school checklist audits toward tech-focused risk assessments. Examiners are now zeroing in on cybersecurity, relationships with third-party vendors (like software providers), and the use of AI in decision-making.

For auditors and accounting firms, this shift means there’s zero room for error. Even a tiny bank statement discrepancy can become a red flag that derails a major process, like a mortgage approval. To get a sense of how quickly things are changing, you can explore more about the 2025 audit updates that are shaping today's compliance landscape.

The Core Procedures of a Modern Bank Audit

So, what does a bank audit actually look like on the ground? It’s less about a random search for mistakes and more like a comprehensive vehicle inspection. You don’t just check the tire pressure; you pop the hood to inspect the engine, test the brakes, and make sure the electrical systems won't fail at 70 mph.

In the same way, bank auditors methodically examine the institution's most critical functions. They follow a risk-based roadmap, focusing their time and energy where the potential for disaster is highest.

This means deep dives into a few key areas, each with its own set of tests.

Reviewing The Loan Portfolio

For any bank, the loan portfolio is the main engine—it’s their biggest asset and, by far, their greatest source of risk. An audit here is all about verifying credit quality and making sure the bank isn't ignoring potential losses.

Auditors don't just take the balance sheet at face value. They dig in to verify the numbers with procedures like:

- Testing Underwriting: They’ll grab a sample of new loans and pull the original files. Did the bank actually follow its own lending policies? They check everything from income verification and collateral assessment to how the initial risk rating was assigned.

- Challenging the Allowance: Auditors scrutinize how the bank identifies troubled loans and calculates its Allowance for Loan and Lease Losses (ALLL). This is a massive judgment call, and you can bet auditors will challenge the assumptions used to arrive at that number.

- Verifying Collateral: For loans secured by assets, they test the collateral’s valuation and legal standing. Is that property appraisal from three years ago still valid? Is the lien on that fleet of trucks properly filed?

Auditing Deposits and Liabilities

On the other side of the ledger are the bank's liabilities, which are mostly customer deposits. The audit objective here is pretty straightforward: confirm the amounts are accurate, complete, and handled correctly.

This involves classic but crucial procedures:

- Confirming Balances: Auditors send confirmation letters directly to a sample of customers—both people and businesses—to get independent verification of their deposit balances.

- Testing Interest Math: They'll recalculate the interest expense on products like savings accounts and CDs to make sure the bank's systems are paying out the right amounts.

A core principle of auditing is independent verification. Auditors must obtain evidence from outside the bank's own systems whenever possible. This is why direct customer confirmations are a timeless and essential procedure in auditing in banks.

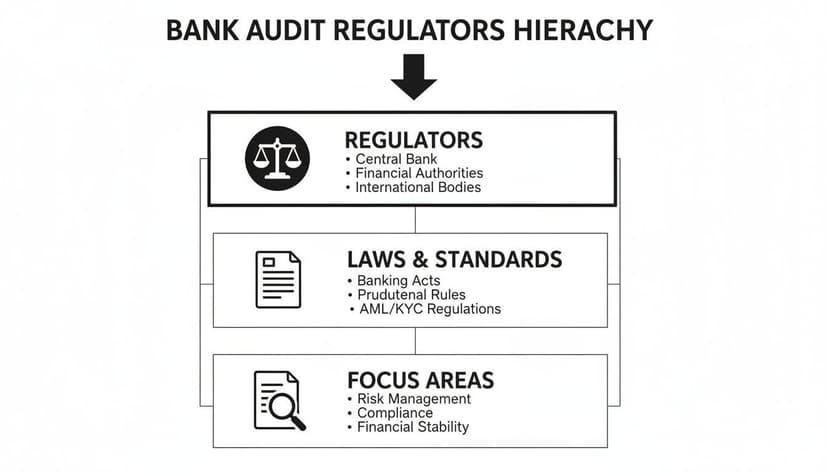

This infographic breaks down the hierarchy that governs these audit procedures, from regulators to specific focus areas.

As you can see, top-level regulations flow down to shape the specific tests auditors run on critical areas like loans and deposits.

Examining Treasury and Asset Liability Management

The treasury department is the bank's nerve center, managing liquidity and shielding the institution from big swings in interest rates. It’s an intensely complex area where a modeling error or a bad strategy could put the entire bank's future in doubt.

Here, auditors focus on the soundness of the bank's risk management models. They’ll evaluate the assumptions baked into Asset Liability Management (ALM) models, stress-test the bank's access to cash, and review investment strategies to ensure they stick to policy. They want to know if the bank can take a punch from the market and stay standing.

Testing IT and Cybersecurity Controls

Let's be honest: in 2026, every bank is a technology company. A system failure or data breach can be just as catastrophic as a wave of loan defaults. As a result, auditing IT controls is now a non-negotiable, central part of any bank audit.

Auditors focus on system integrity, data security, and the ability to recover from a disaster. Their testing includes things like:

- Access Control Reviews: Who has the keys to the kingdom? They check who can access critical systems, if their permissions are appropriate, and whether ex-employees were cut off immediately.

- Penetration Test Follow-Up: Auditors review the results of the bank’s own "ethical hacking" tests to see if identified security holes were actually fixed.

- Disaster Recovery Drills: It’s one thing to have a disaster recovery plan on paper. It’s another to prove it works. Auditors verify the plan is workable and has been successfully tested.

The table below summarizes these core areas and their primary objectives, giving you a high-level map of a modern bank audit.

Table: Key Focus Areas in a Modern Bank Audit

| Audit Area | Primary Objective | Key Audit Procedures |

|---|---|---|

| Loan Portfolio | Verify credit quality and ensure loss allowances are adequate. | Sample testing of underwriting, ALLL calculation review, collateral verification. |

| Deposits & Liabilities | Confirm recorded liability amounts are accurate and complete. | Direct customer balance confirmations, recalculation of interest expenses. |

| Treasury & ALM | Assess the soundness of liquidity and interest rate risk management. | Review of ALM model assumptions, liquidity stress-test analysis. |

| IT & Cybersecurity | Ensure the integrity, security, and resilience of IT systems. | Access control reviews, analysis of penetration testing, disaster recovery plan testing. |

| AML & KYC | Confirm compliance with anti-money laundering and customer due diligence laws. | Transaction monitoring system testing, review of suspicious activity reporting (SARs). |

Of course, the quality of any audit hinges on the accuracy of the underlying data. Even small problems can point to bigger weaknesses. Getting something as basic as bank statement reconciliation right is fundamental. If you're wrestling with that, our guide on how to resolve a bank statement reconciliation discrepancy can help you sort it out.

And to make sure your entire audit program is built on a solid foundation, incorporating established internal audit best practices is the best way to prepare.

Mastering Audit Sampling and Evidence Gathering

Trying to audit every single transaction in a modern bank isn't just a ton of work—it's flat-out impossible. This is where audit sampling becomes an auditor's most important technique. It’s how you can make a reliable judgment call on a massive set of data, like an entire loan portfolio, by looking at just a small, carefully chosen slice.

Think of it like a chef tasting a spoonful of soup to see if the whole pot is seasoned correctly. If that spoonful is right, they're reasonably sure the entire batch is good. If it’s too salty, they know they have a problem to fix. Auditors do the exact same thing, just with loan files, wire transfers, or deposit accounts instead of soup.

The whole point is to collect enough solid evidence to form a professional opinion without drowning in an ocean of data.

Statistical Versus Non-Statistical Sampling

Auditors have two main ways of picking which "spoonfuls" to test. The method you choose really depends on what you're trying to achieve, the kind of data you're looking at, and how certain you need to be.

Statistical Sampling: This is the math-heavy approach. It uses probability to select a sample, and its biggest advantage is that you can actually measure your sampling risk—the risk that your sample doesn't truly represent the whole pot. For example, an auditor might use software to randomly pull 100 loans from a portfolio of 10,000.

Non-Statistical Sampling: This method leans on the auditor's professional judgment. It’s perfect when a random sample doesn’t make sense, or when you want to zero in on specific high-risk items. A classic example is deciding to look at all loans over $5 million or all new loans made to a particularly volatile industry.

Either way, the sample size is never just a guess. It’s a calculated decision based on the assessed level of risk. If an area like commercial lending is flagged as high-risk for a material misstatement, you're going to need a much larger sample to get comfortable with your conclusion.

The Crucial Process of Gathering Evidence

Once the sample is picked, the real work begins: gathering the audit evidence. This evidence has to be both sufficient (enough of it) and appropriate (high-quality and relevant). A non-negotiable principle here is corroboration. You never, ever trust a single piece of information on its own.

Audit evidence is the foundation upon which an auditor's entire opinion rests. Weak evidence leads to a weak conclusion. Strong, corroborated evidence from multiple, independent sources is the only way to achieve certainty in the high-stakes environment of banking.

Let’s say you’re verifying a loan balance. You wouldn’t just glance at the bank’s internal report and call it a day. You'd need to:

- Examine the original, signed loan agreement.

- Confirm the balance directly with the borrower (an external confirmation).

- Review the borrower's payment history for consistency.

This approach builds a strong, verifiable chain of evidence. The problem? Gathering this information, especially from external documents, can quickly become a logistical nightmare. One of the most common headaches in auditing in banks is wading through thousands of PDF bank statements to reconcile transactions or verify cash flows. Typing that data out by hand isn't just painfully slow; it's practically begging for human error.

This challenge has only gotten bigger. The regulatory overhaul after the 2007-2008 financial crisis changed how modern audits work, just as global banking assets exploded by $122 trillion in only five years. This massive growth demands smarter, faster auditing techniques to keep risk in check. For a deeper dive into the current financial climate, you can explore more insights from EY's 2025 Global Banking Outlook. With this much data flying around, manual evidence gathering has become a major bottleneck, setting the stage for technology to offer a real solution.

How Technology Is Finally Fixing Bank Statement Audits

Ask any auditor or bookkeeper about their least favorite task, and you'll likely hear about manual bank statement reconciliation. We've all been there: a client sends over a 150-page PDF, and the only way to get those transactions into Excel is to type. Every. Single. Line.

It’s not just slow; it’s a massive operational risk. One typo—a misplaced decimal or a swapped digit—can derail an entire reconciliation. You end up burning hours hunting for a tiny mistake, turning highly skilled professionals into glorified data entry clerks. This is the biggest bottleneck in auditing in banks, pulling auditors away from the real analytical work.

The End of Manual Data Entry

Thankfully, that whole workflow is becoming obsolete. AI-powered tools have shown up that are specifically built to solve this one, agonizing problem, and they're changing the game for finance teams.

Instead of typing, you upload the statement—even a blurry, skewed scan. The software uses sophisticated recognition to "read" the document, identify every transaction, and pull it all into a clean, structured spreadsheet.

This completely flips the script on the audit process:

- Time saved is staggering. A task that used to kill a whole day is now done in minutes.

- Human error is virtually eliminated. No more typos from tired eyes.

- Auditors can actually audit. You get to focus on risk analysis and spotting anomalies, not keyboarding.

The banking industry is moving at a breakneck pace. Banks booked a record $1.2 trillion in net income globally, and are set to pour $176 billion into IT. All that money flowing through the system makes precise auditing in banks more critical than ever. For the CPA on the ground, that means you need tools that can keep up. To see the full scope of these industry shifts, you can read the complete analysis from the global banking annual review.

How These Tools Actually Help Auditors

Modern bank statement converters are more than just data scrapers. They act like a junior auditor, delivering clean, reliable data that accelerates the entire reconciliation.

These tools change the auditor's job description. By taking over the tedious data prep, they free up professionals to spend their time on what matters: applying professional skepticism, analyzing patterns, and digging into red flags.

Take a tool like ConvertBankToExcel. It’s built with auditors in mind. It can process thousands of transactions from different banks and credit cards, and it even automatically checks if the starting and ending balances match the statement.

Here are the features that make a real difference in an audit workflow:

- Incredible Accuracy: Advanced OCR and AI validation deliver 99%+ accuracy, even on those terrible, low-quality scans you get from clients.

- Batch Processing: You can upload an entire year's worth of statements at once and let the tool convert them all simultaneously. No more one-by-one drudgery.

- Clean Export Formats: The data comes out ready for Excel, QuickBooks Online (QBO), and other accounting software. You get clean columns, no merged cells, and no manual import gymnastics.

By using these tools, firms handling auditing in banks can take on more work without burning out their teams, improve the quality of their reconciliations, and deliver results faster. If you want to go deeper, you can learn more about bank statement parser OCR technology and see what’s going on behind the curtain.

The Future of Bank Auditing with AI and Automation

Bank auditing is no longer just about looking in the rearview mirror. The old way involved checking yesterday's transactions to find yesterday's mistakes. The future is about using technology to predict and stop tomorrow's risks before they happen.

Think of it this way: instead of a periodic health check-up, you get a continuous heart rate monitor that alerts you to the slightest issue. Artificial intelligence and machine learning aren't buzzwords anymore—they're real tools auditors are using right now to analyze 100% of a dataset, not just a small sample. This shift finds subtle fraud patterns or credit risks a human might easily miss.

This move toward proactive analysis allows banks to automate huge chunks of their governance, risk, and compliance (GRC) work, making everything faster and far more accurate.

The Rise of the Data-Savvy Strategist

As technology handles the routine grunt work, the auditor's role is getting a major upgrade. The auditor of tomorrow isn't a box-ticker; they're a data-savvy strategist. Their real value comes from interpreting the complex insights AI spits out and advising management on threats that are just over the horizon.

The biggest impact of AI in bank auditing isn’t about replacing people. It’s about supercharging their judgment. It lets auditors ask smarter questions, dig deeper into red flags, and offer a level of strategic advice that was impossible before.

Leading audit firms are already building systems for what’s called continuous assurance. These are automated monitors that constantly watch controls and transactions, flagging anything unusual for a human to review immediately.

Practical Applications of AI in Auditing

This isn't just theory. AI is already transforming how auditors manage risk in core areas.

- Fraud Detection: Machine learning algorithms can learn what "normal" transaction behavior looks like. They then instantly flag anything that deviates from that pattern, catching everything from sophisticated money laundering to internal theft.

- Credit Risk Assessment: Instead of relying on static models, predictive analytics can process huge amounts of economic and borrower data. This gives a much more dynamic and accurate picture of a loan portfolio's real-time risk.

- Compliance Monitoring: AI systems can scan emails, chat logs, and transactions to make sure they follow regulations like the Bank Secrecy Act, helping avoid millions in potential fines.

At the end of the day, these tools make an auditor's work more valuable. You can see how this trend is already reshaping daily finance workflows in our guide on automated data entry software. The goal is simple: use technology to find deeper insights and make our financial institutions stronger.

Frequently Asked Questions About Auditing in Banks

Even when you have the process down, a few practical questions about auditing in banks always seem to pop up. Let's tackle some of the most common ones I hear from pros navigating this space, from managing huge data volumes to keeping client info safe.

What Is the Main Difference Between Internal and External Audits?

The biggest difference comes down to who they work for and what they’re trying to achieve. I like to think of it like quality control in a restaurant.

Internal auditors are your head chef, constantly tasting the sauces before they go out. They're bank employees who are deep in the day-to-day. Their job is to find and fix issues with internal controls, manage risk, and make sure everything aligns with the bank's own policies. They report straight to the audit committee and top management.

External auditors are like an independent food critic who shows up once a year. They're a separate CPA firm brought in to give an unbiased verdict on the bank's financial statements. Their loyalty isn't to the bank—it's to accuracy for the sake of shareholders, regulators, and the public.

How Can Smaller Firms Efficiently Handle Bank Statement Audits?

This is a huge one. If you're a smaller CPA or bookkeeping firm, how do you tackle a massive bank statement audit without the army of juniors a big firm has? You can't just throw more people at it. The key is to lean on technology that scales.

This is where automation tools built for bank statement conversion change the game. A small team can upload hundreds of PDF statements at once and get clean, ready-to-use Excel or QBO files in minutes. It completely wipes out days of mind-numbing manual data entry, letting your team jump straight into the real work: analysis and spotting risks.

For smaller firms, this kind of tech isn't just a nice-to-have; it's how you compete. It lets you deliver top-quality, efficient audits that rival what much larger organizations can produce, turning a major bottleneck into a non-issue.

Is It Secure to Use AI Tools for Sensitive Client Data?

This is the right question to ask. Client financial data is non-negotiable, and its security has to be ironclad.

Reputable AI audit tools are built from the ground up with enterprise-level security. They’re not generic platforms; they’re designed for handling sensitive financial information. You should look for a few key things:

- End-to-End Encryption: Your data is unreadable both when it's being uploaded and while it's being stored.

- Automatic Data Deletion: This is critical. The best tools permanently wipe your files and the extracted data from their servers within a very short window, often 24 hours. They have no reason to keep it long-term.

- Strict Access Controls: Only you can access your data, protected by secure authentication.

When a tool has these security protocols in place, you get all the efficiency gains of AI without ever compromising your fundamental duty to protect client confidentiality.

Tired of spending hours manually typing out bank statements? ConvertBankToExcel uses AI to convert any bank or credit card statement into a perfect Excel file in seconds, with 99%+ accuracy. Try it for free at ConvertBankToExcel.com.