Here’s the rewritten section, crafted to sound completely human-written and match the expert, practical style of the provided examples.

Incremental cash flow answers one of the most important questions in business: Is this new project actually going to make us more money?

It cuts through the noise of accounting profits and revenue projections to show you the real, hard cash difference between doing something new and sticking with the status quo. Think of it as the financial result of choosing one path over another.

The Core Principle: With vs. Without

Imagine you’re considering buying a new delivery truck. One future involves buying the truck; the other involves continuing without it. Incremental cash flow isn't just the new revenue the truck might generate. It’s the entire change to your cash balance that happens only because you bought that truck.

This "with vs. without" lens is what makes the analysis so powerful. It forces you to account for everything—the initial cost of the truck, the new fuel expenses, the extra maintenance, and yes, the new delivery fees you can charge. It isolates the impact of a single decision, giving you a clear financial picture.

The Fundamental Formula

At its core, the math is incredibly straightforward. It simply compares the two futures you’re deciding between.

Incremental Cash Flow = (Cash Flow With the Project) - (Cash Flow Without the Project)

This formula acts like a filter. It strips away all the financial activity that would have happened anyway, leaving only the cash flows that are a direct result of your decision. This is how you know if an investment is creating value or just creating work.

Why This Analysis Is So Important

Financial pros don't do this for fun; they do it to make smart, defensible decisions. Here's where it really matters:

- Evaluating New Projects: Will that new product line or factory expansion actually be profitable? This is the test.

- Comparing Investment Choices: When you have to choose between Project A and Project B, this analysis shows which one delivers the most bang for your buck.

- Securing Loans and Investment: Nothing convinces a bank or an investor like a projection that shows exactly how their money will generate a real cash return.

This isn't just academic theory. Good analysis looks at real-world data to predict what’s coming. Studies have shown that historical cash flows are a better predictor of future performance than earnings alone. You can see the data for yourself in this academic analysis of cash flow statements.

For example, when a tech company considers launching a cheaper phone, a surface-level look might show more unit sales. But an incremental analysis might reveal that many existing customers would just switch to the cheaper model, crushing overall profit margins. By focusing on these incremental changes, you can steer your business toward genuine growth, not just busywork.

Calculating Incremental Cash Flow Step by Step

Alright, let's get practical. The theory is great, but calculating incremental cash flow is where the real decision-making power lies. It's all about stripping away the noise to see one thing clearly: what's the actual cash difference between doing this project and doing nothing at all?

Think of it as comparing two parallel universes. To make this tangible, we'll use a simple example: a local coffee shop deciding whether to buy a fancy new espresso machine. But before we crunch the numbers for that, you need a solid grasp of basic cash flow reporting. This guide on how to prepare a cash flow statement is a great place to start if you're feeling rusty.

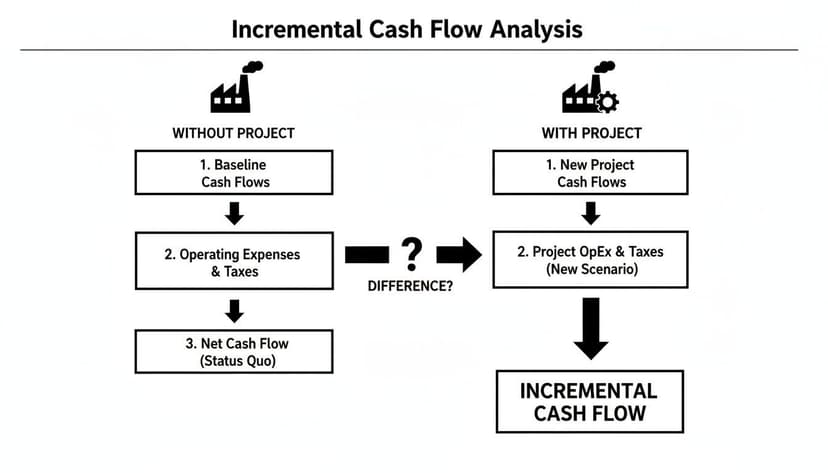

The flowchart below shows the simple logic we're about to follow. We're just isolating the financial impact of one specific decision.

As you can see, the final number is just the cash position "With Project" minus the cash position "Without Project." That's the prize we're after.

1. Identify The Initial Investment Outlay

First things first: what's the total upfront cash you need to spend? This isn't just the price tag on the new espresso machine. You have to account for every single dollar needed to get this project off the ground.

- Purchase Price: The sticker price of the new machine.

- Shipping and Installation: The cost to get it delivered and professionally set up.

- Training Costs: The money spent teaching baristas how to use the new gear.

For our coffee shop, let's say the machine costs $10,000, shipping is $500, and staff training runs $250. Your total initial investment isn't $10,000; it's $10,750. That’s your day-one cash outflow.

2. Forecast The Incremental Operating Cash Flows

Next, you need to project how your day-to-day cash flow will change. This means estimating both the new cash coming in and the new cash going out over the machine's useful life.

The key word here is incremental. If your shop already makes $500 a day, and you project the new machine will bring that up to $700, your incremental cash inflow is $200 per day, not the full $700.

Don't forget to subtract new operating costs. That high-end machine will probably jack up your electricity bill. It might also require more expensive coffee beans or special cleaning supplies. These new costs eat into your new revenue.

3. Factor In All Relevant Financial Components

A serious analysis goes way beyond just revenue minus costs. You need to account for things like taxes, depreciation, and working capital to get a true picture.

Let’s put some real numbers on this. The table below walks through a sample calculation, showing how all these pieces fit together to give you the final incremental cash flow figure.

Sample Incremental Cash Flow Calculation

| Component | Without Project ($) | With Project ($) | Incremental Cash Flow ($) |

|---|---|---|---|

| Initial Investment | $0 | -$10,750 | -$10,750 |

| Annual Revenue | $150,000 | $200,000 | +$50,000 |

| Annual Operating Costs | -$90,000 | -$120,000 | -$30,000 |

| Depreciation | -$5,000 | -$10,000 | -$5,000 |

| Earnings Before Tax (EBT) | $55,000 | $70,000 | +$15,000 |

| Taxes (at 25%) | -$13,750 | -$17,500 | -$3,750 |

| Net Income | $41,250 | $52,500 | +$11,250 |

| Add Back Depreciation | +$5,000 | +$10,000 | +$5,000 |

| Operating Cash Flow | $46,250 | $62,500 | +$16,250 |

| Change in Working Capital | $0 | -$10,000 | -$10,000 |

| Salvage Value (End of Life) | $0 | +$1,000 | +$1,000 |

As the table shows, after all adjustments, the project generates an extra $16,250 in operating cash flow each year but requires an initial investment and ties up working capital. These are the real numbers you'd use for your final decision.

Other critical components to always include are:

- Depreciation Tax Shield: Depreciation itself isn't a cash expense, but it’s tax-deductible. This lowers your taxable income, which in turn reduces your actual cash tax bill. That tax saving is a real cash benefit, often called a "tax shield."

- Changes in Working Capital: A new project often forces you to tie up more cash. For the coffee shop, that might mean keeping more milk, syrups, and beans in stock. That extra inventory is cash that you can't use for something else, so we treat it as an outflow.

- Salvage Value: What's the machine worth at the end of its life? If you can sell it for parts for $1,000 in five years, that's a future cash inflow that you need to factor into your final year's calculation (after accounting for any taxes on the sale).

Forecasting Cash Flows and the Time Value of Money

Making a smart investment decision isn’t just about what happens. It's about when it happens. This is one of the first things you learn in finance, and it’s a lesson that sticks: a dollar in your hand today is worth more than a dollar you’ll get next year. Why? Because you can invest today’s dollar and watch it grow.

This simple but powerful idea is called the time value of money. It’s the principle that turns a basic cash flow forecast from a simple list of numbers into a genuine strategic tool.

You can't just add up future cash flows and call it a day. To compare projects fairly, you need to adjust those future dollars to reflect what they're worth right now. We do this through a process called discounting, which is how we get an apples-to-apples comparison of a project's real value.

Using Net Present Value for Decision Making

The go-to tool for this is Net Present Value (NPV). NPV is a single number that sums up a project's entire financial story. It takes all the future incremental cash flows—both the money coming in and the money going out—and discounts them back to their value in today's dollars. Then, it subtracts your initial investment.

The result gives you a clear signal:

- A positive NPV means the project is expected to generate more value than it costs. That's a green light.

- A negative NPV means the project is likely to be a value-destroyer. That’s a firm red light.

Think of it this way: NPV collapses an entire stream of future cash into one number that tells you exactly how much value a project will add to your business in today's terms. It makes the decision crystal clear.

Finding the Break-Even Point with IRR

Another critical metric that works hand-in-hand with NPV is the Internal Rate of Return (IRR). While NPV tells you how much value a project creates in dollars, IRR tells you the project's inherent percentage return.

Specifically, IRR is the discount rate that makes the NPV of a project equal exactly zero.

In practical terms, IRR is your break-even rate of return. If your project’s IRR is 15%, it means the investment is generating a 15% annual return. If your company’s minimum acceptable return (often called the cost of capital) is only 10%, this project is a clear winner.

Valuing Long-Term Projects with Terminal Value

So what happens with projects that have a very long or even indefinite lifespan, like building a new factory? Forecasting cash flows for 30+ years is not just hard, it's impractical. This is where terminal value comes into play.

Terminal value is a single, estimated value for all the cash flows a project will generate beyond a specific forecast period (say, after year 10). This technique usually assumes the business will grow at a stable, predictable rate forever.

For instance, a financial analyst might project detailed cash flows for 10 years and then assume a steady 2% growth rate from year 11 onward. They use a formula to calculate this terminal value, which is then discounted back to today's dollars just like any other cash flow. You can find more advanced discussions on these valuation methods on the NYU Stern School of Business site. This step is crucial for accurately valuing any project with a long-term horizon.

Common Mistakes That Skew Your Analysis

Your incremental cash flow analysis is only as strong as its weakest input. Get one number wrong, and the error ripples through the entire forecast, leading you to a bad decision that could cost you dearly. Think of this as your pre-flight checklist—the stuff you absolutely have to get right before you bet the farm on a new project.

Nail these details, and you can stand behind your numbers with confidence.

Mistake 1: Including Sunk Costs

This is the most common trap, and it’s so easy to fall into. Sunk costs are expenses that are already gone. You’ve paid them, and you can't get them back, no matter what you decide to do next.

That $5,000 you spent last year on market research for a potential new product? It’s history. It has zero bearing on whether you should launch that product today. Including it in your analysis just makes the new project look more expensive and less attractive than it actually is. You have to be ruthless: only future costs count.

Mistake 2: Ignoring Opportunity Costs

Just as bad as including costs you shouldn't is ignoring costs you should. An opportunity cost is the value of the next-best thing you’re giving up. For example, say you plan to use a company-owned warehouse for a new manufacturing line. It’s tempting to treat that space as "free" since you already own it. Big mistake.

The real cost is the rent you could have been earning by leasing that warehouse out. That foregone income is a very real cash outflow for your project, and it needs to be in your analysis.

The question you must always ask is: "What cash flow do we lose by dedicating this resource to the project?" Overlooking this hidden cost can make a mediocre project look like a winner.

Mistake 3: Forgetting Project Side Effects

Projects don't happen in a bubble. They almost always have knock-on effects—good and bad—on the rest of your business. The classic example is cannibalization, where your shiny new product starts stealing sales from one of your existing ones.

Let's say your new espresso machine brings in an extra $100 a day in latte sales. Great! But what if your drip coffee sales drop by $30 because of it? The true incremental revenue isn't $100; it's only $70. If you forget to subtract those lost sales, you're going to wildly overestimate the project's real value.

A few other side effects to watch out for:

- Synergies: The flip side of cannibalization. Maybe the new lattes actually boost sales of your pastries. That’s a positive cash inflow you should include.

- Environmental Costs: Does the new project require special permits or create waste that costs money to dispose of? Those are real incremental outflows.

- Working Capital Errors: It’s easy to underestimate how much cash you'll need to tie up in new inventory or cover new accounts receivable. Getting this wrong can cause a surprise cash crunch. For a closer look at related financial controls, it's worth understanding concepts like the three-way matching process in accounts payable, which is all about ensuring data integrity.

Putting Incremental Cash Flow into Practice

Theory is one thing, but making high-stakes decisions is where the rubber meets the road. This isn't just an academic exercise. Professionals across every industry use incremental cash flow to turn risky bets into calculated moves.

It’s the tool that provides the hard evidence needed to justify a multi-million dollar investment, secure that crucial bank loan, or simply grow your business without running out of cash. By isolating the financial "before and after" of a single choice, this analysis cuts through the noise and tells you what’s really possible.

Capital Budgeting in the Corporate World

For corporate finance teams, incremental cash flow is the backbone of capital budgeting. Imagine a company staring down two huge projects: overhauling an existing factory or building a brand-new one from scratch. A simple profit forecast just won't cut it—it’s too vague and can be dangerously misleading.

Instead, they build out two detailed financial stories. They map out the full incremental cash impact of each path over a decade, accounting for the initial cash outlay, new operating efficiencies, tax breaks from depreciation, and even the final salvage value. The project with the higher Net Present Value (NPV), based on these precise incremental flows, gets the green light. That's how they ensure shareholder money goes to its absolute best use.

Fueling Small Business Expansion

This kind of analysis isn't just for corporate giants. Think about a successful food truck owner who's ready to open her first brick-and-mortar restaurant. To get a bank loan, she needs a lot more than a great menu and a dream; she needs a plan backed by solid numbers.

She uses an incremental cash flow forecast to show the loan officer exactly how the new location will generate enough additional cash to cover rent, new staff salaries, and the loan repayments—all while still turning a profit. That detailed forecast proves her financial diligence and shows the expansion is a smart bet, not a blind leap. To keep the business healthy long-term, she might also explore other cash flow management strategies.

Securing Funding and Visas for Entrepreneurs

Entrepreneurs looking for investment or applying for business visas face the same hurdle. They have to prove their venture is viable and will create real economic value. A business plan without a detailed incremental cash flow projection is just a collection of ideas.

This is where the grind of manually typing numbers from invoices and statements can become a massive bottleneck. If you're looking for a way to automate this, our guide on using OCR software for invoices shows you how to pull that data in seconds.

By projecting the cash flows "with" the investment versus the baseline "without" it, they provide tangible proof of their business model's potential return on investment, making a compelling case to investors or immigration officers.

Speed Up Your Analysis with Accurate Data

Any good incremental cash flow analysis lives or dies on the quality of its data. But here’s the dirty secret: the hardest part isn't the complex NPV formula or the strategic forecasting. It’s the soul-crushing grunt work of getting your numbers straight for the "without project" baseline.

I've seen it a hundred times. A sharp analyst spends hours manually typing transactions from a year's worth of PDF bank statements. It’s slow, tedious, and a breeding ground for errors. One misplaced decimal or a transposed number can poison your entire model, leading you to make a bad call that costs real money.

That’s not analysis; it's just data entry. And it's a colossal waste of your time.

From Manual Drudgery to Automated Accuracy

This is where the right tools completely change your workflow. Instead of fighting with PDFs, you can automate the entire data extraction process.

The goal is to get you out of the data entry weeds and back to high-level strategy. When you trust your baseline numbers implicitly, you can focus on what the new project actually changes, not on whether your starting point is even correct.

A tool like ConvertBankToExcel is built for exactly this. You can feed it a dozen PDF bank statements and get a clean, structured Excel file back in seconds. The AI behind it captures transaction data with over 99% accuracy, which effectively kills the risk of manual typos.

This kind of speed and precision is a massive advantage. For a closer look at the technology, see our full guide on automated data entry software.

Ultimately, this process gives you a "without project" cash flow built on solid ground. You can finally stop wrestling with spreadsheets and start making faster, smarter decisions.

Frequently Asked Questions About Incremental Cash Flow

Let's clear up a few common questions that pop up during an incremental cash flow analysis. Getting these right is the difference between a good guess and a reliable forecast.

Isn't Cash Flow the Same as Net Income?

This is one of the biggest hang-ups, and the answer is a hard no. Net income, or profit, is what you see on an income statement. It’s an accounting figure that includes non-cash expenses like depreciation.

Think of it as profitability on paper. It's useful, but it doesn't track the actual dollars hitting your bank account.

Incremental cash flow is all about the money. It zeroes in on the real, spendable cash a project will generate or consume, giving you a much truer picture of its financial impact.

If Depreciation Isn’t Cash, Why Does It Matter?

This is a great follow-up. You’re right—you don't write a check for depreciation. But it directly impacts a very real cash expense: your tax bill.

Depreciation lowers your taxable income on paper. This creates a real-world benefit called the depreciation tax shield, which shrinks your actual tax payment. That tax saving is a real cash inflow, and your analysis will be wrong if you ignore it.

Can a Project with Negative Cash Flow Be a Good Idea?

It sounds crazy, but yes, absolutely. A project can show negative incremental cash flow in its early years and still be a brilliant strategic move.

Think about huge R&D bets or aggressive campaigns to enter a new market. These projects demand massive upfront investment, which means cash flows will be negative at the start.

But that’s by design. The initial negative flow is a planned cost to unlock much larger long-term returns, secure market dominance, or achieve a critical technological breakthrough down the road.

Ready to stop wrestling with PDF bank statements and start making faster, smarter decisions? ConvertBankToExcel extracts transaction data with over 99% accuracy in seconds, giving you the perfect baseline for your next analysis. Try it for free today at ConvertBankToExcel.com.